Model your CD now: Open the free CD Calculator — end balance, after-tax interest, donut chart, and annual or monthly accumulation schedules in a two-column layout.

What is a certificate of deposit?

A certificate of deposit (CD) is a timed savings product: you deposit a lump sum for a set maturity date and earn a quoted interest rate. Banks and credit unions use CDs to fund lending and operations. For savers, CDs trade liquidity for predictability — you know the rate and maturity date upfront on a traditional fixed CD.

Terms often range from three months to five years. Longer CDs may pay more but lock your money longer. This guide pairs with our CD Calculator, which projects end balance, total interest, and schedules from your deposit, rate, compounding choice, and optional tax rate.

How to use the CD calculator

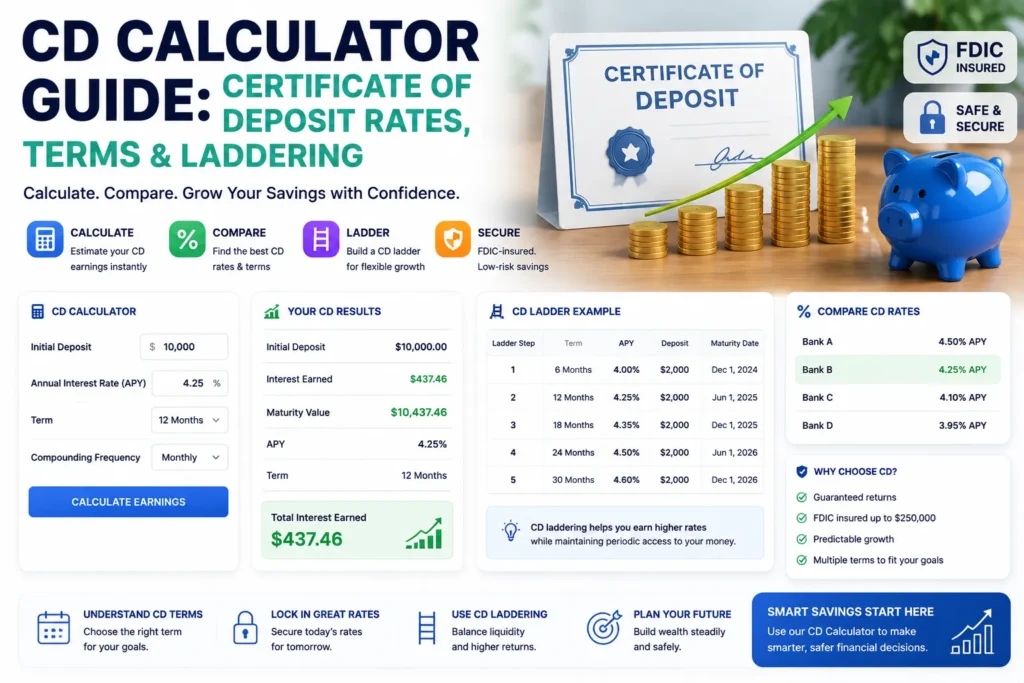

- Enter your initial deposit and the bank’s quoted interest rate.

- Pick compound frequency — most U.S. CDs are advertised as APY (annually).

- Set years and months for the CD term.

- Add a marginal tax rate if the CD is taxable (skip for IRA CDs).

- Click Calculate and switch between annual and monthly accumulation schedules.

Compare two bank offers by running each scenario separately, or convert APR to APY first with the APY Calculator.

APY vs APR on CDs

APY (annual percentage yield) includes compounding within the year. APR (annual percentage rate) is the nominal rate before compounding frequency is applied. Banks usually market CDs with APY because it is the more accurate picture of what you earn. A 5.00% APY compounded monthly beats a 5.00% APR compounded monthly — always normalize before choosing.

FDIC and NCUA protection

CDs at FDIC-member banks are insured up to $250,000 per depositor, per bank, per ownership category. Credit unions offer parallel coverage through NCUA. Insurance protects against institution failure, not market loss or early-withdrawal penalties.

Shopping for CDs

Compare APY, minimum deposits, maturity, and early-withdrawal penalties across institutions. Online banks often lead on rate; local banks may bundle relationship perks. Brokered CDs broaden issuer choice but read call features and fees.

CD ladder explained

Instead of one 3-year CD, split funds into 1-, 2-, and 3-year rungs. When the 1-year matures, reinvest at the long end or spend. Laddering balances yield with periodic access — especially useful when rates are rising.

Early withdrawal penalties

Cashing out before maturity typically forfeits a slice of interest — sometimes principal if penalties exceed accrued interest. Callable and liquid CDs are exceptions with their own rules. Model the hold-to-maturity case in the calculator; penalties are institution-specific.

CD types at a glance

| Type | Key trait |

|---|---|

| Traditional | Fixed rate, fixed term, predictable maturity value |

| Bump-up | One chance to raise rate if market yields climb |

| Callable | Bank may redeem early; often starts with higher yield |

| Liquid | Limited penalty-free withdrawals; lower APY |

| Brokered | Purchased via brokerage; traded on secondary market |

When CDs make sense

- You have a fixed horizon and want principal protection.

- You are building a conservative sleeve near retirement.

- You prefer known returns over variable savings rates.

When you need frequent access or rising-rate flexibility, compare the Money Market Account Calculator or Savings Calculator. For multi-year investing with ongoing contributions, use the Compound Interest Calculator. For linear interest without compounding, see the Simple Interest Calculator.

CD and savings calculators on ShoutingNow

- CD Calculator — fixed-term deposit growth with tax and accumulation schedules

- CD Calculator Guide — what CDs are, FDIC insurance, laddering, and alternatives

- APY Calculator — convert APR and APY before comparing bank quotes

- Money Market Account Calculator — liquid savings with optional contributions

- Savings Calculator — deposits, withdrawals, and inflation-adjusted contributions

- Compound Interest Calculator — full investment growth with flexible contribution modes