Run your numbers now: Open the free Paycheck Calculator — hourly or salary, all 50 states, overtime, 401(k), and a take-home breakdown chart after you click Calculate.

Why your take-home pay is smaller than your salary

When a job offer lists $60,000 per year, that is almost never what hits your checking account each week. Employers withhold money for federal income tax, Social Security, Medicare, and (in most states) state income tax before issuing pay. Voluntary deductions — health insurance, FSAs, and 401(k) contributions — reduce your check further, though pre-tax benefits also lower taxable wages.

Understanding that gap helps you budget rent, debt payments, and savings without surprise on the first payday. A paycheck calculator lets you model the split before you accept an offer or change your W-4.

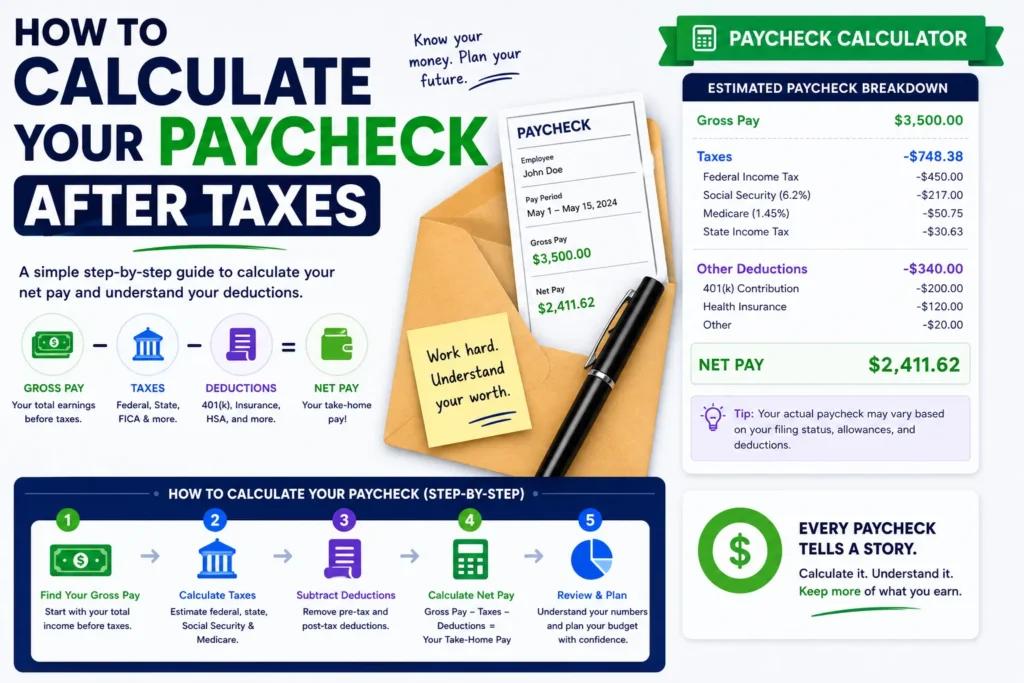

Gross pay vs net pay

Gross pay is total earnings for the period before deductions. Net pay (take-home) is what remains. The relationship is simple in concept:

- Net = Gross − Taxes − Benefits

In practice, taxes are layered: federal brackets apply to taxable wages after the standard deduction, FICA is a flat percentage on gross (with a Social Security cap), and state rules differ from Texas (no wage income tax) to California or New York (progressive state withholding).

Step 1: Find gross pay for the period

Salary workers

Divide annual salary by pay periods:

- Weekly: annual ÷ 52

- Bi-weekly: annual ÷ 26

- Semi-monthly: annual ÷ 24

- Monthly: annual ÷ 12

Example: $60,000 salary paid weekly → $60,000 ÷ 52 ≈ $1,153.85 gross per check before overtime or deductions.

Hourly workers

Multiply hourly rate × hours worked in the period. A hourly paycheck calculator is essential when hours vary — restaurant, retail, and gig-adjacent W-2 roles rarely use fixed salary math.

Overtime

Non-exempt employees often earn 1.5× the regular rate after 40 hours in a workweek (rules vary by state and industry). Double time may apply on holidays or after a second overtime threshold. Overtime lifts gross pay and therefore taxes — it is not “all take-home.”

Paycheck & payroll resources on ShoutingNow

- Paycheck Calculator — estimate take-home pay by state with federal tax, FICA, benefits, and overtime

- How to Calculate Your Paycheck After Taxes — this guide with formulas and examples

- Percentage Calculator — raises, deferrals, and quick percent math

- Sales Tax Calculator — see how percentage taxes apply to a price

- Commission Calculator — variable pay on top of base wages

Step 2: Subtract FICA (Social Security and Medicare)

Nearly every W-2 paycheck includes FICA:

- Social Security: 6.2% on wages up to the annual wage base (IRS adjusts yearly)

- Medicare: 1.45% on all wages; an extra 0.9% may apply on high earners

These are not optional for most employees. They fund Social Security retirement benefits and Medicare hospital insurance.

Step 3: Estimate federal income tax withholding

Federal withholding follows your Form W-4 (filing status, dependents, other income, deductions, extra withholding). The IRS publishes percentage and wage-bracket methods in Publication 15-T. Employers use those tables — you do not calculate brackets manually each payday.

For planning, remember:

- Standard deduction reduces taxable income before brackets apply

- Pre-tax 401(k) and health premiums lower wages subject to federal tax

- “Married filing jointly” uses wider brackets than single

Step 4: Add state (and remember local) taxes

State paycheck tax is the biggest variable when comparing offers:

- Texas, Florida, Nevada, Washington, Wyoming — no broad state wage income tax

- California, New York, New Jersey, Illinois, Pennsylvania, Ohio — regular state withholding each period

City taxes (NYC, Philadelphia, Detroit, etc.) can add another layer not always shown in basic calculators. Always read your pay stub for local lines.

Step 5: Account for benefits

Medical, dental, vision, HSA, and traditional 401(k) contributions are often pre-tax, shrinking taxable wages. Roth 401(k) deferrals are post-tax for income tax but still reduce your net check. Modeling a paycheck with 401(k) before open enrollment helps you pick a deferral rate that balances retirement savings and cash flow.

Worked example: Texas weekly paycheck

Single filer, $60,000 salary, weekly pay, Texas, no benefits, no overtime:

- Gross per week ≈ $1,153.85

- Social Security ≈ 6.2% of gross

- Medicare ≈ 1.45% of gross

- Federal income tax — depends on W-4; typically the largest variable line

- Texas state tax — $0 on wages

Use our Paycheck Calculator with the same inputs to see a full breakdown chart. Cross-check federal withholding against IRS Publication 15-T and FICA rates on SSA.gov.

Gross up: when you need a target net

Sometimes you know the take-home you need — covering rent plus student loans, for example — and must find the gross offer required. Gross up (net-to-gross) reverses the math. Open the Gross Up Calculator tab and enter your desired net for the period.

Quick tips for accurate estimates

- Match pay frequency to how you are actually paid

- Update filing status after marriage or dependents

- Re-run the calculator when you change 401(k) % or health plans

- Use the Percentage Calculator for raise math; use the Sales Tax Calculator as a parallel for how percentage rates stack on a base amount

Disclaimer

This article and the linked calculator provide educational estimates — not tax, legal, or payroll advice. Confirm withholding with your employer and a qualified professional before making financial decisions.